Table of Content

Conventional loans that don’t meet these guidelines are known as nonconforming loans. That can include loans that exceed the limits set by the FHFA or have looser credit score requirements . Conventional loans are open to virtually all qualified borrowers.

The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. Refinance disclosure - By refinancing the existing loan, the total finance charges may be higher over the life of the loan. Bankrate’s editorial team writes on behalf of YOU – the reader. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy.

Benefits Of A VA Loan Vs. Conventional Loan

Because VA mortgages are non-conforming, they must be held by their lender or sold to another – but not Fannie Mae or Freddie Mac. Non-conforming loans also include jumbo loans, Federal Housing Administration loans and U.S. Regardless of your down payment on the VA loan, you’d still end up paying the VA funding fee, whereas you’d be able to avoid paying PMI with a down payment of 20% or higher on a conventional loan. The lack of PMI could result in a lower monthly payment on a conventional loan compared to financing with a VA loan. Housing market conditions, inflation and even the Federal Reserve all factor into current mortgage rates.

This may influence which products we write about and where and how the product appears on a page. Here is a list of our partners and here's how we make money. We believe everyone should be able to make financial decisions with confidence. Some sellers are nervous about accepting VA loans because of the increased home inspection and appraisal criteria.

Mortgage Requirements For VA Loans Vs. Conventional Loans

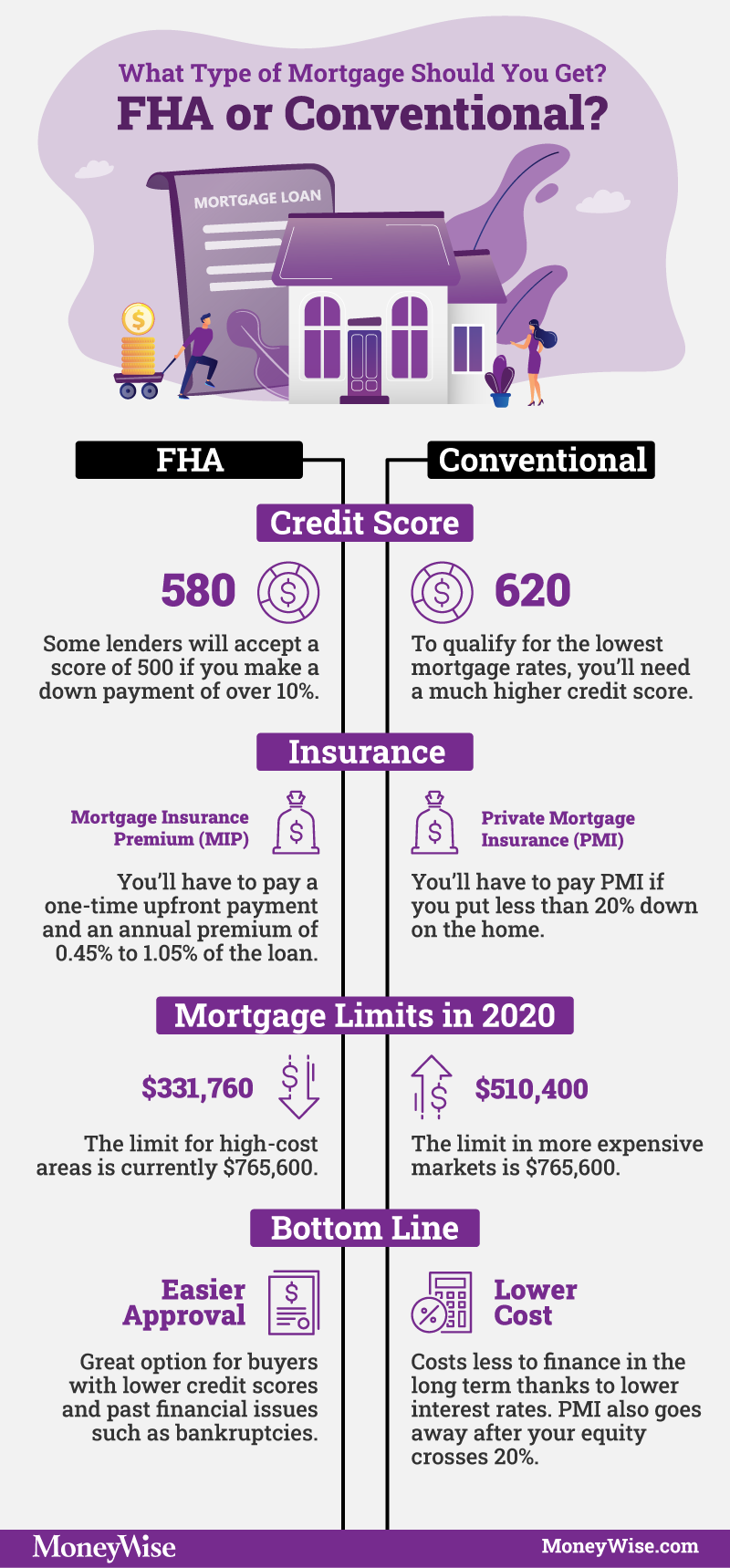

Upfront MIP of 1.75% of the loan amount and monthly MIP amounts are usually required. In this article, you'll learn what you need to know about conventional, FHA-insured, and VA-guaranteed loans as of 2022. In most cases, a VA loan is a fantastic option to use if it is available to you due to your military connections.

However, the requirements for each appraisal will differ based on the rules and regulations set forth by either the Department of Veteran Affairs or the Department of Housing and Urban Development. For more information and any questions, please contact one of our experienced mortgage professionals to help prepare for your upcoming appraisal. This is a common question that many borrowers ask because an appraisal can make or break the deal for their potential home. Lenders will use an appraisal to help determine a home’s actual value based on its condition, location, and any other features it may have. It also helps ensure that the property meets all health and safety standards, which are commonly referred to as the Minimum Property Standards. All of these factors help determine whether or not the home’s contract price is accurate, and it helps the mortgage lender decide if they will give a borrower a loan for that specific property.

Comparing VA Loans to Conventional Loans

Although conventional loans are available to all types of borrowers, they do have their share of cons. However, conventional loans can also include favorable terms based on the lender. Lenders charge this fee to cover the cost of processing the loan. It generally costs 0.5% –1% of the loan’s total amount, and you pay it as part of your closing costs.

FHA loans are government-backed by the Federal Housing Administration and generally have more flexible qualification criteria than conventional loans. VA loans are also guaranteed by the federal government through the U.S. Department of Veterans Affairs and cater to active-duty military, veterans and surviving spouses. A VA loan is a mortgage option that is fully backed by the U.S. As a result of this guarantee, VA mortgages require no private mortgage insurance and make the qualification process easier. They typically have more favorable interest rates and conditions than other loan types, including conventional loans.

Mortgage insurance

They’re referred to as “streamline” refinances because they have fewer documentation requirements than regular refinances and typically don’t require a home appraisal. If you’re looking to buy a home and are eligible to apply for both an FHA loan and a VA loan, you might be unsure of which one you should get. Each type has unique features and benefits, so the loan that’s best for you will likely depend on your financial situation and needs. Whether you are getting a conventional or VA loan, both typically require an appraisal.

If you’re eligible, VA loans are an excellent option for home buyers, offering competitive interest rates and requiring no down payment. Conventional loans that conform to Fannie Mae or Freddie Mac guidelines are limited to a maximum loan amount (up to $625,500 for a single family residence) that depends on where the home is located. Some non-conforming conventional loans known as jumbo loans have no loan limit.

Debt-to-income ratios are calculated by dividing all your monthly expenses by your gross monthly income. Lenders utilize this ratio to measure a borrower’s ability to make monthly home loan payments. In addition, insurance is usually required if the down payment is less than 20%. Share ThisIf you plan to buy a home, you are undoubtedly considering the various types of loans to finance your purchase. VA loans have a specific range of interest rates, benefits and qualification requirements.

Furthermore, you may have difficulty in transferring a conventional mortgage loan, making it a significant commitment when compared to transferable mortgages. If both VA loans and conventional loans are available to you, compare their requirements. You may find one fits your situation better than the other.

Instead, they guarantee the loans for the lenders that fund them. Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication.

No comments:

Post a Comment